Keep on top of your business and in front of the competition

Grow your business with confidence using real-time sales, revenue and customer loyalty reporting

See how Insights makes for better business

Real time reporting

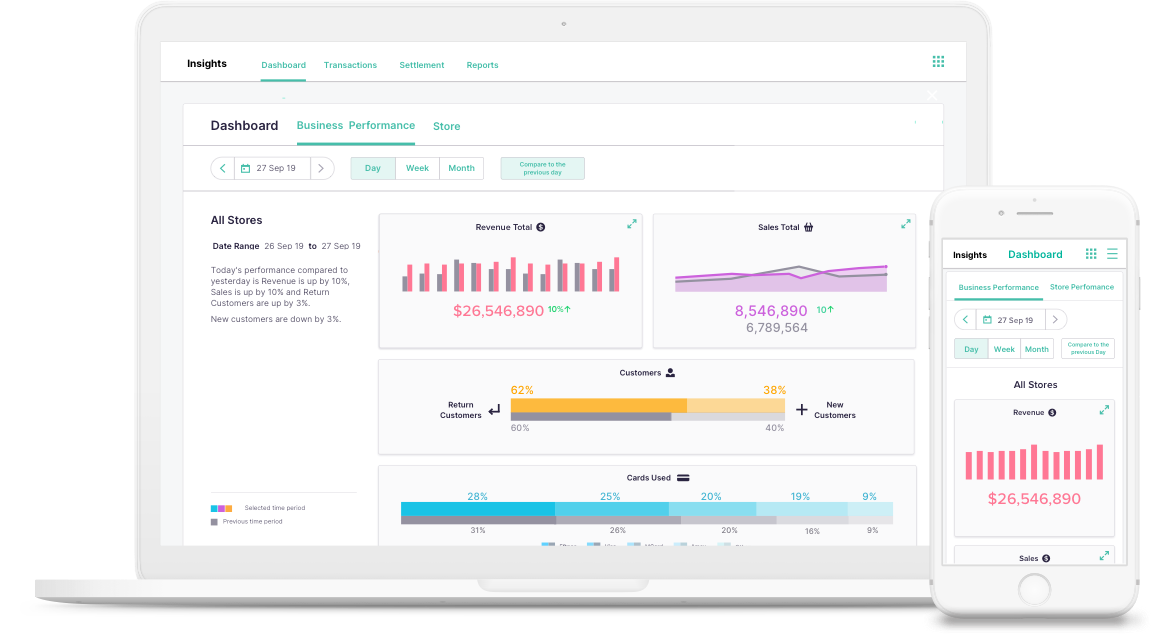

Live, real time reporting of sales, revenue, customer numbers, and top cards used. Available from anywhere on mobile or desktop.

Total Business Performance & Store Performance

Access to real time reporting across all stores or at individual store level.

New vs Return Customers

Customer loyalty reporting to track how many customers have been to the store before, and how many visited for the first time. No set up required, with numbers updated in real time.

Compare to previous day and week

Visibility of how sales, revenue and customer numbers compare to the previous day or the previous week. Available for the whole business and individual stores.

Empowering all Kiwi businesses to make better business decisions

Access powerful performance reports that until now has been out of reach for every day Kiwi businesses

See how Insights makes for better business

New to Insights? Register through the link below and get started today.